[ad_1]

Editor’s be aware: This can be a recurring put up, commonly up to date with new info.

Credit score scores are three-digit numbers, often between 300 and 850, representing the theoretical probability you’ll repay a mortgage on time. They’re additionally a bit mysterious, and that’s no accident. The key credit-scoring corporations, FICO and VantageScore, preserve their formulation secret. Whereas there are issues we do know, solely a handful of individuals know the precise recipe that’s used to generate a credit score rating.

However, credit-scoring corporations launch sufficient info that consultants can largely decide how these numbers are calculated. Right here’s what you could learn about how credit score scores work.

Credit score rating fundamentals

Credit score-scoring fashions use an individual’s credit score historical past from one of many three main shopper credit score bureaus: Experian, Equifax or TransUnion. Earlier than credit score scores existed, a lender must pull a duplicate of your total credit score report after which analyze it to find out your creditworthiness. However now, they will go off a single quantity.

Associated: FICO vs. VantageScore: What’s the distinction and why does it matter?

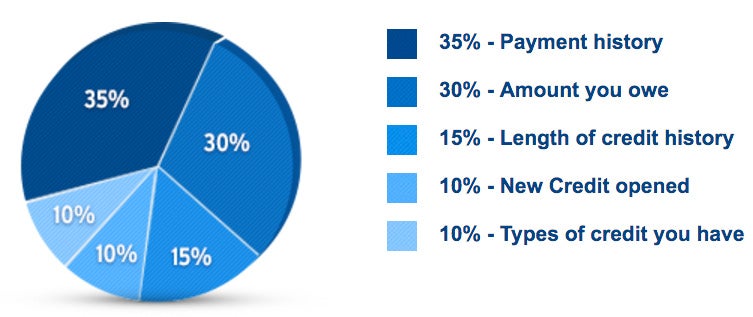

What makes up your credit score rating

FICO is comparatively forthcoming in regards to the general components that make up its credit-scoring fashions:

Cost historical past: 35% of a FICO rating includes your cost historical past. When you get behind in making mortgage or credit score account funds, the longer and more moderen the delinquency, the better the adverse impression in your credit score rating.

Quantities owed: 30% is predicated on the relative scale of your present debt. Particularly, your debt-to-credit ratio is the entire of your money owed divided by the entire quantity of credit score you’ve been prolonged throughout all accounts. Lenders typically prefer to see a debt-to-credit ratio under 30%, however the decrease, the higher.

Size of credit score historical past: 15% is predicated on the common age of all accounts in your credit score historical past. This turns into a big issue for these with little or no credit score historical past, corresponding to younger adults, current immigrants and anybody who has largely prevented credit score. It can be an element for individuals who open and shut accounts inside a really brief interval.

Join our day by day publication

New credit score: 10% is set by your most up-to-date accounts. Opening too many accounts inside a short while body might need a adverse impression in your rating, because the scoring fashions will interpret this as an indication of potential monetary misery.

Credit score combine: 10% is said to what number of various kinds of credit score accounts you’ve, corresponding to mortgages, automotive loans, credit score loans and retailer cost playing cards. Whereas having a bigger mixture of credit score accounts is best than having fewer, nobody recommends taking out pointless loans simply to diversify credit score and increase your rating.

Associated: Find out how to test your credit score rating free of charge

Find out how to increase your credit score rating the standard means

Pay your payments on time persistently

Persistently paying your payments on time is crucial means to enhance your credit score rating. Fortunately, most lenders received’t report delinquencies lower than 30 days previous, and plenty of received’t even report funds which can be 30 to 60 days late. However when you get past 60 days, every late cost will dramatically have an effect on your credit score rating.

Most of your accounts will let you take additional steps to make sure you’ll pay your payments on time, like organising alerts and reminders and computerized funds. Benefit from these choices to assist make sure you’ll by no means miss a cost.

Associated: 6 issues to do to enhance your credit score

Decrease your debt-to-credit ratio

Your debt-to-credit ratio is the entire quantity of debt you’ve divided by the entire quantity of credit score you’ve been prolonged throughout all accounts. The 2 methods to lower your debt-to-credit ratio are to lower your debt and to extend your credit score.

Because of this making use of for a brand new bank card can really assist your credit score rating. Rising your out there credit score, both by present accounts or by opening a brand new account, ought to lower your debt-to-credit ratio — when you don’t tackle extra debt. That is additionally why, when you plan on canceling a bank card, you’ll wish to transfer the road of credit score on that card to a different card to maintain your general line of credit score as excessive as potential.

Associated: Credit score utilization ratio: What’s it and the way it impacts your credit score rating

Keep away from opening new credit score traces too shortly

After making on-time funds and decreasing your debt-to-credit ratio, the subsequent necessary factor you could bear in mind is to not open up plenty of new bank card accounts or different loans in a brief period of time. Card issuers don’t wish to mortgage cash to somebody who seems to be looking for plenty of new loans, as that may very well be an indication of economic instability.

Associated: How does making use of for a brand new bank card have an effect on my rating?

Right errors

One other means you may enhance your credit score rating is to right any errors you discover in your credit score historical past.

You’ll be able to request credit score stories free of charge from the three main credit score bureaus and test for errors. When you discover any, request to have these errors corrected, as they may considerably impression your credit score rating.

Associated: Find out how to right errors in your credit score report

Ask for forbearance

Whenever you’ve made a mistake that’s affected your credit score report and rating, it’s potential to ask the lender to take away the adverse info. Merely name or write the lender, clarify your mistake and politely request that they amend your credit score historical past to take away the file.

In our expertise, this works finest for minor errors on an account with an in any other case spotless cost file. And earlier than asking for forbearance, guarantee your account is not delinquent.

Widespread misconceptions about credit score scores

There’s a fast repair for adverse credit

Like advertisements for magical tablets that supposedly will let you shed some pounds with out eating regimen and train, loads of folks declare to have found (and can attempt to promote you) a fast repair for adverse credit.

The reality is that you need to pay your payments on time and carry little or no debt. You will have an ideal credit score rating when you do these two issues and have a big credit score historical past. However when you’ve got a file of late funds and a excessive stage of debt, it can take a while and constant good credit score habits to tug your rating up.

Associated: 3 actual methods to spice up your credit score rating in 30 days

Fewer bank cards are higher

Many people at TPG have quite a few bank card accounts. In response to listening to that, some conclude that our credit score should be horrible and are stunned to be taught that we’ve got glorious credit score not regardless of our quite a few accounts — however due to them.

When managed responsibly, every account provides constructive info to your credit score historical past and helps you keep a excessive credit score rating. So when you’ve got little-used accounts with no annual charge, there’s actually little motive to shut them.

Have a look at it from the lender’s perspective: Would you fairly provide a brand new line of credit score to somebody with a really restricted file of paying again loans or somebody with a really in depth historical past of managing a number of credit score traces responsibly?

Associated: Right here’s why I’ve 19 bank cards

0% is the best credit score utilization ratio

By by no means utilizing your bank cards or by paying off your balances earlier than the assertion closes, it’s potential to have a credit score report that reveals 0% utilization. But it surely’s really higher to have a really low utilization ratio versus 0% utilization.

Once more, the credit-scoring fashions favor those that use credit score responsibly over those that don’t use it in any respect.

Backside line

Figuring out how your credit score rating works is extremely necessary. And as you may see, having the next rating is right, so understanding the ins and outs of how it’s decided may also help you make higher monetary choices.

It’s also by no means too late to attempt to enhance your rating. In case you are able the place your credit score rating is low, there are lots of issues you are able to do to maneuver that rating up the dimensions. Whereas it received’t occur in a single day, just some modifications can go a good distance and have an effect on whether or not or not you’ll be authorised for a brand new line of credit score.

[ad_2]